¿Tienes dudas?

What Is the Fixed Asset Turnover Ratio?

One common variation—termed the “fixed asset turnover ratio”—includes only long-term fixed assets (PP&E) in the calculation, as opposed to all assets. The Fixed Asset Turnover Ratio measures how effectively a company uses its fixed assets to generate revenue. Total asset turnover measures the efficiency of a company’s use of all of its assets. Such efficiency ratios indicate that a business uses fixed assets to efficiently generate sales. Low FAT ratio indicates a business isn’t using fixed assets efficiently and may be over-invested in them.

Total Asset Turnover Calculation Example

Several factors impact how companies calculate and interpret their asset turnover ratio. However, it is important to remember that the FAT ratio is just one financial metric. The dynamics of total asset turnover are different for various industries.

How to use FAT Ratio to optimize your business?

- Thus, to calculate the asset turnover ratio, divide net sales or revenue by the average total assets.

- This means that Company A uses fixed assets efficiently compared to Company B.

- This concept is important to investors because they want to be able to measure an approximate return on their investment.

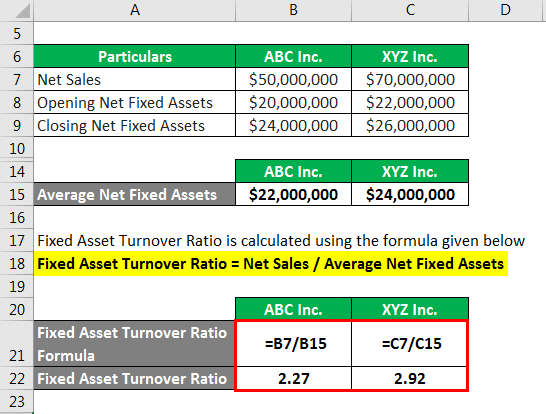

- Therefore, Y Co. generates a sales revenue of $3.33 for each dollar invested in fixed assets compared to X Co., which produces a sales revenue of $3.19 for each dollar invested in fixed assets.

- In this example, Caterpillar’s fixed asset turnover ratio is more relevant and should hold more weight for analysts than Meta’s FAT ratio.

- For example, retail or service sector companies have relatively small asset bases combined with high sales volume.

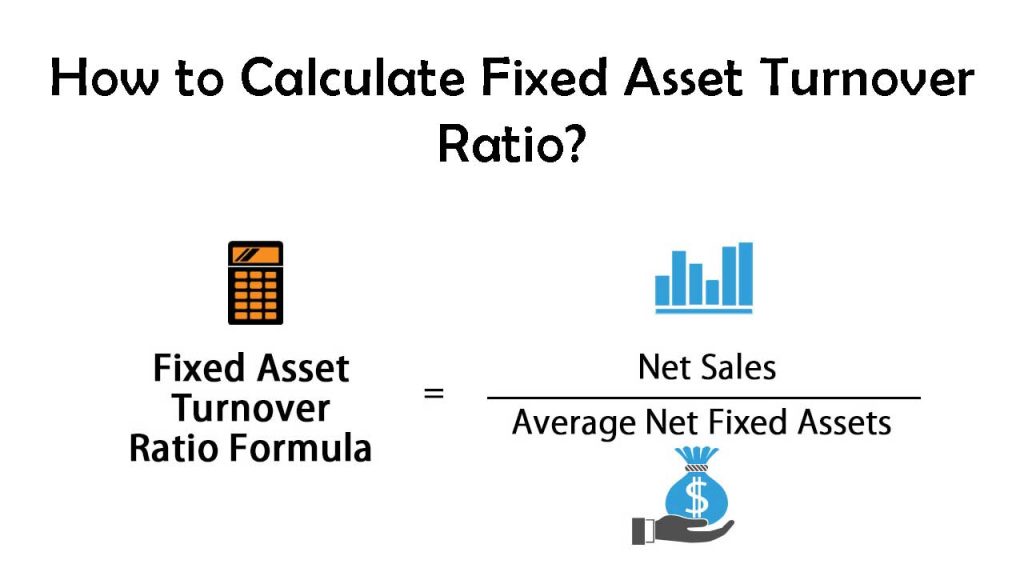

By improving your fixed asset turnover ratio, you can optimize your return on investment in these critical assets. The fixed asset turnover ratio formula is calculated by dividing net sales by the total property, plant, and equipment net of accumulated depreciation. The asset turnover ratio can also be analyzed by tracking the ratio for a single company over time. As the company grows, the asset turnover ratio measures how efficiently the company is expanding over time; especially compared to the rest of the market. Although a company’s total revenue may be increasing, the asset turnover ratio can identify whether that company is becoming more or less efficient at using its assets effectively to generate profits.

Importance of the Fixed Asset Turnover Ratio for Your Business

The fixed asset turnover is a ratio that can help you to analyze a company’s operational efficiency. Because of this, it’s crucial for analysts and investors to compare a company’s most current ratio to both its historical ratios as well as ratio values from peers and/or the industry average. The FAT ratio measures a company’s efficiency to use fixed assets for generating sales. We have prepared this total asset turnover calculator for you to calculate the total asset turnover ratio. The total asset turnover ratio tells you how much revenue a company can generate given its asset base.

Can the fixed asset turnover be negative?

A higher turnover ratio indicates greater efficiency in managing fixed-asset investments. Analysts and investors often compare a company’s most recent ratio to historical ratios, ratio values from peer companies, or average ratios for the company’s industry. The fixed asset turnover ratio is intended to isolate the efficiency at which a company uses its fixed asset base to generate sales (i.e. capital expenditure).

Future Trends and Forecasts in Fixed Asset Turnover Ratios

The asset turnover ratio measures the efficiency of a company’s assets in generating revenue or sales. It compares the dollar amount of sales to its total assets as an annualized percentage. Thus, to calculate the asset turnover ratio, divide net sales or revenue by the average total assets. One variation on this metric considers only a company’s fixed assets (the FAT ratio) instead of total assets. The asset turnover ratio helps investors understand how effectively companies are using their assets to generate sales.

A company may have record sales and efficiently use fixed assets but have high levels of variable, administrative, or other expenses. Companies with higher fixed asset turnover ratios earn more money for every dollar they’ve invested in fixed assets. A company’s asset turnover ratio will be smaller than its fixed asset turnover ratio because the denominator in the equation is larger while the numerator stays the same.

As each industry has its own characteristics, favorable asset turnover ratio calculations will vary from sector to sector. Companies can artificially inflate their asset turnover ratio by selling off assets. This improves the company’s asset turnover ratio in the short term as revenue (the numerator) increases as the company’s the basics of reit taxation assets (the denominator) decrease. However, the company then has fewer resources to generate sales in the future. The asset turnover ratio calculation can be modified to omit these uncommon revenue occurrences. It is the gross sales from a specific period less returns, allowances, or discounts taken by customers.

When comparing the asset turnover ratio between companies, ensure the net sales calculations are being pulled from the same period. Therefore, Y Co. generates a sales revenue of $3.33 for each dollar invested in fixed assets compared to X Co., which produces a sales revenue of $3.19 for each dollar invested in fixed assets. Therefore, based on the above comparison, we can say that Y Co. is a bit more efficient in utilizing its fixed assets. Companies with cyclical sales may have low ratios in slow periods, so the ratio should be analyzed over several periods. Additionally, management may outsource production to reduce reliance on assets and improve its FAT ratio, while still struggling to maintain stable cash flows and other business fundamentals.